NO ‘WAY’ NO! SAVE DATAPULSE!!!

NO ‘WAY’ NO! SAVE DATAPULSE!!!

Dear Fellow ShareholdersThe requisitioned EGM by the family of former Datapulse Technology chairman and co-founder Ng Khim Guan seeking to replace four directors on the Company’s Board and re-evaluate its diversification strategy is being scheduled for 20 April 2018. It is a mammoth task for the family whose combined stake at about 16% is small relative to the new controlling shareholder’s 29% shareholding.

As a group of concerned shareholders whose interests are aligned with the rest of the minority shareholders – of which there are more than 9000 of us and who together hold 55% of the shares in the Company – we are naturally troubled by recent developments in the Company, as have been reported in the newspapers as well as various articles and commentaries on the Company that have been written by experts in corporate governance and company law matters. We are concerned about the Company’s future well-being and whether the minority shareholders’ rights and interests will be protected and safeguarded.

Although we minority shareholders are actually the ‘majority shareholder’ of the Company, but because of the fragmented nature and spread of our shareholdings, it is extremely difficult for us to organize and assert ourselves. With the requisition for the EGM by the family of the former chairman and co-founder, we have a chance now to decide whether to keep the existing directors and to put the Company’s diversification plan on hold. We should carefully consider the proposed resolutions put forward by the requisitioning shareholders, attend the EGM, ask questions and vote to safeguard and protect our interests.

Since the start of the Datapulse saga in early November last year, we have been following the newspaper reports and the published articles by Associate Professor Mak Yuen Teen of the NUS Business School, National University of Singapore. As many of us are laymen, we may not fully appreciate the many things that have taken place since the current directors were appointed, but Professor Mak’s articles have helped us to understand these matters better. Having read all of Professor Mak’s articles, we feel concerned about the corporate events that have unfolded and how the actions of the Board might have adversely affected minority shareholders’ rights and interests. Professor Mak’s articles can be found at his website at www.governanceforstakeholders.com. Specifically, Professor Mak has provided his views and comments on the resolutions to be tabled for voting at the EGM. This gives a neutral perspective for shareholders to consider the matters of concern that will arise at the EGM, and to better understand how to protect their interests as well as the interests of the Company. This article can be found at http://www.governanceforstakeholders.com/2018/02/15/datapulse-technology-update-on-egm/

Accordingly, our positions on the issues are as follows:

- We are for removing the entire Board comprising Mr Low Beng Tin, Mr Thomas Ng DerSian, Mr Rainer Teo Jia Kai and Mr Wilson Teng.

- We are for reconstituting the Board with the new appointments of Mr Ng Boon Yew, MrLoo Cheng Guan, Ms Ng Bie Tjin @ Djuniarti Intan and Mr Koh Wee Seng. Brief credentials of the proposed directors are attached.

- We reject the diversification into Proposed Consumer Business and/or Proposed Investment Business.

- We are for invoking the ‘buyback guarantee’ for the acquisition of ‘Wayco’ which in substance is an interested/connected party transaction and was done without proper due diligence.

- We reject the Board’s diversification plan as it seeks to build on the ‘Wayco’ acquisition. WE SAY NO ‘WAY’ NO.

- We support the requisitionists’ call to stop further diversification for now until after a careful study by the reconstituted new Board. If we see nothing workable or viable, we will petition to distribute all of the cash as we want our money back!

If this were to materialize shareholders will stand to see the CASH of about 38 CENTS for EACH SHARE owned.

Every vote counts, since we are facing a majority 29% shareholder. We urge you to join us to attend the coming EGM. If you are unable to attend the EGM and vote, it is critical for you to submit a proxy form to allow your vote to be counted in our favour.

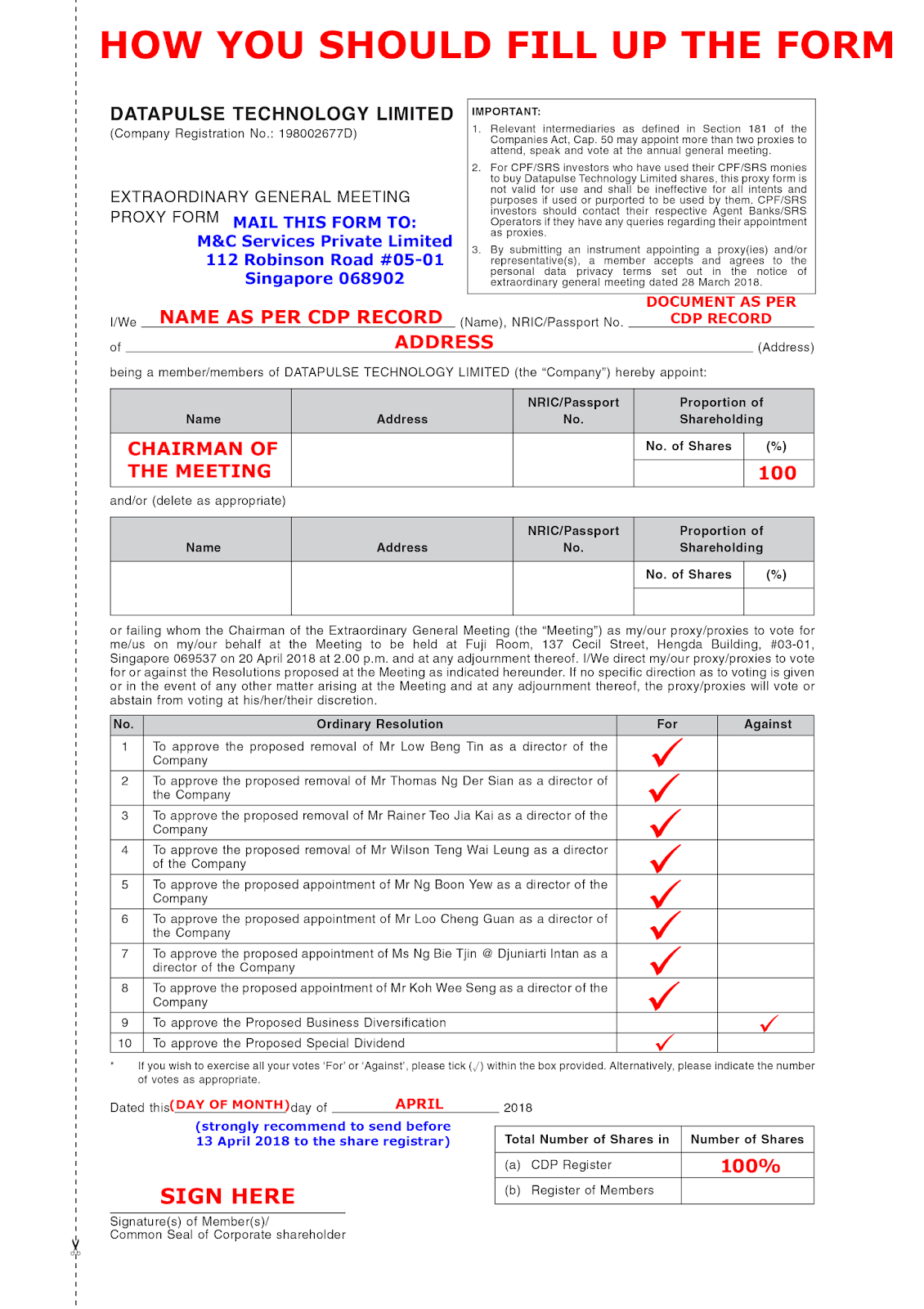

We have attached a sample PROXY FORM on how you should fill up the form, to proxy the Chairman of the Meeting with your voting clearly marked under the “FOR” column to support the 8 resolutions for removals and appointments and under the “AGAINST” column to reject the resolution for diversification. Please contact us by email at savedatapulse@gmail.com at least a week before the EGM to help verify that your proxy form is properly completed, before it is sent to the Company’s Share Registrar office for registration by the deadline on Tuesday, 17 April 2018, i.e. not less than 48 hours before the time scheduled for holding the EGM.

For more information, please contact us by email at savedatapulse@gmail.com

We look forward to your support to vote your shares to safeguard and protect the interests of all shareholders and TO PROTECT THE EIGHTY FOUR (84) MILLION DOLLARS OF OUR MONEY! Thank you.

With best wishes,

Chew Ah Kong

For and on behalf of a Group of Concerned Shareholders

各位胜达公司的股东们

持胜达科技约16%股权的Uniseraya控股和黄渼媜,发出申请通知,要求召开的特别股东大会,定在4月20日举行。议题是罢免非执行主席兼董事刘明镇及另外三名董事,及提名四位新董事重组董事局。

现胜达公司董事局,经股份转手之后成立,新的第一大股东拥有股权29%。胜达公司在现董事局成立一天后,未详细审核,以350万元收购生产护发产品和化妆品等的马国 Wayco,该公司去年上半年净盈利仅5万3000元左右。

我们一群小股东,对于现董事局成立以后的收购及拟定的未来发展计划,非常担忧,我们认为现董事局的收购计划,影响到一般小股东的利益,从事件发展到现在,国大教授Mak Yuen Teen在媒体与个人网站 www.governanceforstakeholders.com 针对事件重点发表了他的看法,让我们更加眀确了解到我们小股东的利益受到影响。他也建议小股东针对股东大会议题如何投票,全力支持发出审请通告的股东Uniseraya的议題。

胜达股东结构,我们小股东拥有55%。但是这股份是分散在超过9000人手上。这注定我们小股东要团结积极参与,以出席特别股东大会投票或授权投票方式,大声的表态我们的意愿,才能改变董事局,决定公司的发展方向。不然这拥有29%的第一大股东就能决定公司的发展方向。

我们认为我们的利益是与Uniseraya黄渼媜是一条线上的,因此呼吁其他小股东也与我们站在同一线上,支持他们,因为我们分散的股份是不足发出申请通知要求召开特别股东大会的。Uniseraya的这个申请通知要求开特别股东会,我们才有机会让现有的董事局知道我们是不赞同他们的收购方式,也不支持由他们来决定公司的方向。

我们支持罢免刘明镇的非执行主席和董事职务,以及黄德贤、张嘉凯和Wilson Teng的董事职务。

我们支持委任黄渼媜和Uniseraya控股建议委任的吳文友,吕清源,许伟盛三人为董事。

我们反对转形护发产品和化妆品及投资策略。

公司拥有现款8400 万($84,000,000), 每股约三十八分($0.38),如果公司沒有找到好的項目,我们觉得这钱还是发还给我们股东更加稳当。

不要觉得我们的股份微小,起不了作用,每一股的声音都很重要,每一股都会給予我们的成功增加希望,我们恳请每一个小股东都站出来,如果不能出席股东大会,请一定要签下授权投票委讬书,如您支持我们,请根据我们的建议填写委托书投票。如果有任何咨询,请务必发送电子邮件至savedatapulse@gmail.com。

让大家凝聚小股东力量,一起站出來保护我们的$84,000,000吧!

招玡匡

代表一群小股东

|

| Click here to download the image |

CREDENTIALS OF PROPOSED DIRECTORS

Ng Boon Yew

Mr Ng is a Chartered Accountant who was in KPMG for 25 years. He became a Partner of the firm in 1984 until his retirement in 2000. He also served as KPMG's Chairman of the Professional Practice Committee, headed its Banking Practice and was the partner in charge of Corporate Finance Services.Since Mr Ng's retirement, he has served as Adviser to the Singapore Technologies Group. He then came out of retirement to be the Group Chief Financial Officer of Singapore Technologies Pte Ltd from July 2002 to December 2004. He is currently Chairman of Raffles Campus Group.

Mr Ng was a member of the Corporate Finance Committee under the Financial Sector Review Group, chaired by then Deputy Prime Minister Lee Hsien Loong. He was also appointed Chairman of the Disclosure and Accounting Standards Committee, established by the Ministry of Finance, Monetary Authority of Singapore and the Attorney-General’s Chamber.

Mr Ng was a member of the Council on Governance of Institutions of a Public Character (IPCs), which establishes rules and regulations for IPCs in Singapore. He served as a Board Member of the National Kidney Foundation (NKF) and Chairman of its Audit Committee; he also served as Chairman of its Finance Committee. He was reappointed to the Board of NKF on 1 July 2017 and currently also serves as Chairman of its Finance Committee. He was awarded the Public Service Star in the 2004 National Day Award.

Mr Ng holds various directorships in companies listed on the Stock Exchanges of Singapore and Taiwan, and serves on boards of numerous non-profit organisations, foundations, charities and public and statutory institutions. He was formerly an independent director of Datapulse Technology Limited from 3 September 2001 to 31 July 2013. He was Chairman of the Remuneration Committee and a member of the Audit Committee and Nominating Committee from 3 September 2001 to 5 January 2012, and subsequently from 6 January 2012 to 31 July 2013, he was the Chairman of the Audit Committee and member of the Nominating Committee and Remuneration Committee.

Loo Cheng Guan

Mr Loo founded Vermilion Gate in 2014 and formally launched it in 2016 as an advisory firm to focus on cross-border M&As. He has been non-executive Chairman of 1 Rockstead GIP Fund II Pte Ltd., a private equity fund approved by the Singapore Government under its Global Investors Programme, since 2013. He is also chairman of Precursor Group, a Singapore-based accounting firm and honorary director of Pantheon Assets, a leading multi-family office in China.In addition, he sits on the boards of Valuetronics Holdings Ltd., a SGX-listed EMS company, as an independent director, and of several other private companies including Fortrec Chemicals & Petroleum Pte Ltd, Amalgam Capital Partners Pte Ltd and Brash Asia Pte Ltd. Cheng Guan had previously sat on a number of listed companies in Singapore, China and Canada, including Advance SCT Ltd as independent director and Chairman, Audit Committee and MAP Technology Holdings Ltd as independent director, Grandblue Environment Holdings Ltd and Blackbird Energy Ltd both as non-executive director.

Ng Bie Tjin @ Djuniarti Intan

Ms Ng was with Datapulse Technology Limited for over 22 years and was the Finance Director from January 1994 to November 2014. Apart from overseeing the daily operations of the finance functions including accounting, finance, treasury and capital management, Ms Ng was responsible for administration and implementation of the Group's corporate finance strategies and policies, corporate governance and internal control policies and procedures, investor relations, and identification and evaluation of new business opportunities. She was the key person who pushed for the company to obtain a shareholders’ mandate to diversify into property development.Ms Ng was a director of Datapulse Technology Limited from 7 January 1994 to 30 November 2014, and during that time, was a member of the Nominating Committee.

She is also an independent director of Aspial Corporation Limited from 20 January 2014 and SunMoon Food Company Limited from 31 August 2017. She is also a director of Uniseraya Holdings Pte Ltd from January 2015.

Ms Ng holds a Masters in Business Administration from the University of Southern California.

Koh Wee Seng

Mr Koh is Aspial’s Chief Executive Officer and Executive Director and is responsible for the strategic planning, overall management and business development of the Aspial Group.Since late 1994, when the new management team, led by Mr Koh, took over the reins, Aspial Group has overcome the challenges posed by changing consumer demand by implementing wide-ranging and fundamental changes in its jewellery business. Mr Koh has also successfully led Aspial Group’s diversification into the property business in Singapore, Australia and other countries and financial service business. Mr Koh is also the Non-executive Chairman of Maxi-Cash Financial Services Corporation Ltd, AF Global Limited and World Class Global Limited, which are listed on the SGX-ST.

Mr Koh holds a Bachelor’s degree in Business Administration from the National University of Singapore.

DATAPULSE TECHNOLOGY: RESPONSE TO MISLEADING AND

MALICIOUS DOCUMENT

Published March 31, 2018By Mak Yuen Teen

It has come to my attention that a misleading and malicious document, which includes statements relating to what I have written and me personally, has been distributed to Datapulse shareholders. The writer(s) has chosen the cowardly approach of remaining anonymous.

I realise that this document may not only be aimed at misleading shareholders when they vote at the EGM on April 20, but to distract or discourage me from writing more about Datapulse. I urge minority shareholders of Datapulse not to be swayed and to turn out in force on April 20 to vote out the current directors and appoint the new directors. On my part, I have drafted a response which you can read via this link: http://www.governanceforstakeholders.com/wpcontent/uploads/2018/03/response-to-anonymous-document-2.pdf.

GUIDE TO VOTING ON RESOLUTIONS AT EGM ON 20 APRIL 2018

Excerpts from an article “Is Datapulse Technology holding the EGM at the busiest time of the year?” by Professor Mak Yuen Teen published on February 15, 2018 in his publication series on Governance for Stakeholders at www.governanceforstakeholders.comGiven all that has happened, my view is that shareholders should instruct their proxies to vote against the diversification resolution proposed by the current board (in case SGX does not reject the proposed change in business, which it can under the rules) and vote for all the resolutions proposed by the requisitioning shareholders. The reasons should have been clear from the series of articles I have published. Here is a summary, with some additional information.

Why Mr Low Beng Tin should be removed

Updated with information from Why Low Beng Tin should be removed, published on 29 March 2018, and can be found at http://www.governanceforstakeholders.com/2018/03/29/more-questions-about-the-suitability-of-low-beng-tin-as-a-director/More questions about the suitability of Low Beng Tin as a director

I had previously written several articles where I made reference to the track record of Low Beng Tin, the chairman of Datapulse Technology, who is one of the directors proposed for removal by requisitioning shareholders at the EGM on April 20. I had explained why I support the removal of Mr Low as director and chairman (and the removal of the other directors).For example, Mr Low made wrong disclosures about regulatory actions by SGX and MAS against China Yongsheng, where he was the lead independent director, when he was appointed to the boards of Datapulse, Fuji Offset Manufacturing and Lian Beng. He also provided the wrong answer to the question as to whether there had been a petition for winding-up against any company he had been a director of, for the relevant period covered in the announcement template, when he was appointed to the boards of Datapulse and Fuji Offset (it did not apply in the case of Lian Beng because he joined that board before the winding-up petition was filed).

Whether Mr Low himself made the incorrect disclosures or he relied on others to complete the appointment template for him is, in my view, irrelevant because as a director, he is ultimately responsible. This was made clear by SGX in the case involving Singapore Post (SingPost).

In that case, SingPost had made an incorrect disclosure that no director had an interest in a transaction. After it discovered the mistake, the company, with advice from an external lawyer, decided that no announcement to correct the error was necessary. This was not surfaced to the board. The company only issued the “clarification announcement”, attributing it to an “administrative oversight”, after I had pointed out the incorrect disclosure. SGX did not accept the explanation and reprimanded the company.

SGX said the following: “The board of a company is ultimately responsible for the announcements made by the company and must not abdicate its responsibility to any professionals especially where matters under consideration are not subjective but factual in nature…A company and its board must exercise due care in drafting, reviewing and approving SGXNET announcements. Any error must be promptly escalated to the board’s attention for its deliberation and decision.”

In this case, the incorrect disclosures relate to matters which are factual in nature. The responsibility for the incorrect disclosures, which relate to Mr Low personally, and not to the company, must rest with Mr Low. It would not be reasonable to expect the companies to do the kind of checking that I was doing about disclosures made by directors. The incorrect disclosures remained uncorrected for periods of up to more than two years. Further, when Mr Low was appointed to the Datapulse board, the board said that it was of the view that “Mr Low, being an independent director of several other listed companies, is well versed with listing compliance and corporate governance matters and will be able to contribute to the Board in his role”. With such experience, he should have known the requirement to make accurate disclosures.

Given the reprimand meted out by SGX in the case of SingPost, one would expect that the multiple incorrect disclosures made by Mr Low would likewise attract sanction.

In my earlier articles, I also urged shareholders to consider Mr Low’s track record as a director in the companies that he had been associated with. Other than Datapulse, the SGX-listed companies where he is currently a director are Cosmosteel, Lian Beng and Fuji Offset (he has resigned from China Yongsheng which had attracted the regulatory sanctions). Mr Low was also the founder of OEL Holdings, previously called Oakwell Engineering. Let me reiterate and expand on what has happened in these companies.

In the case of Cosmosteel, Mr Low has been a director since November 2005 and is its independent chairman. Cosmosteel entered the SGX watchlist in June 2017 due to the MTP criteria. In December 2017, it announced that it has made three consecutive years’ of losses. Therefore, it is facing a potential mandatory delisting.

Mr Low joined Lian Beng’s board as an independent director in July 2015, after two independent directors had resigned in a very public dispute with management/controlling shareholders over the remuneration of the executive directors. I published a commentary on the issues relating to the dispute (“Performance bonus may just be the tip of the iceberg,” Business Times, August 25, 2015). Mr Low chairs the nominating and audit committees and is a member of the remuneration committee.

After Mr Low and another new independent director replaced the directors who resigned, Lian Beng’s remuneration continued to be questioned by the Securities Investors Association (Singapore) (SIAS) in its Q&A on annual reports, which also asked questions on other areas. In the area of remuneration, in September 2016, SIAS asked why the remuneration of the directors had increased by 21 percent, from $9.78 million in 2015 to $11.86 million in 2016, even though the group’s net profit had fallen by 20 percent and its profit attributable to shareholders had dropped by 5 percent. The disconnect between profit and remuneration needed explanation because bonus/profit-sharing constitutes a significant part of the remuneration of the executive directors. In September 2017, SIAS again asked several questions. On remuneration, this time it asked why the remuneration of the top eight key executives (excluding the CEO and directors) had only dropped by 1.3 percent when revenues and profit attributable to shareholders had dropped by 37 percent and 48 percent respectively. A number of family members of Lian Beng’s controlling shareholder are among the eight key executives.

What was Lian Beng’s responses to those questions? Nothing. It did not respond at all. Lian Beng is no paragon of corporate governance and communication with shareholders, and remuneration of its executive directors and key management remains a concern, after Mr Low joined as an independent director.

In the case of Fuji Offset, Mr Low joined the board on May 3, 2017, replacing another independent director who had resigned for “health reasons” that day. The controlling shareholder and chairman of Fuji Offset was listed as one of the top 20 shareholders in Datapulse’s 2016 annual report, owning just over 1 percent of Datapulse’s shares. In the 2017 annual report, his stake had increased to about 1.4 percent as of October 9, 2017. It is unclear if he was one of those who sold his shares to Ms Ng Siew Hong.

Fuji’s latest unaudited full year results for the year ended December 31, 2017 shows a loss from continuing operations of $1.08 million, down from a profit of $69,000 in the previous year, while the loss including discontinued operations was $1.23 million, down from a profit of $29,000 the previous year. Tough times may be ahead there it seems. Since Mr Low only joined the board on May 3, 2017, it remains to be seen whether Mr Low would be able to help create shareholder value there.

However, perhaps the company that is most relevant in assessing Mr Low’s performance track record is OEL Holdings. OEL, previously called Oakwell Engineering, is listed on Catalist. Mr Low was founder and director of OEL from September 1984 and became chairman and managing director in July 1992. He relinquished his chairman and managing director role in March 2016, became an executive director, before resigning from the board in October 2016.

I was only able to access the annual reports of Oakwell/OEL online from FY2011 onwards. Based on these, it appears that performance had a turn for the worse from FY2011, when its profit fell by nearly half from $3.7 million in FY2010 to $1.9 million in FY2011 and its cash flows from operating activities went from positive $34 million to negative $34 million. In FY2012, Oakwell reported a net loss of $29 million, although cash flows from operating activities returned to positive territory of $3 million.

In October 2013, Oakwell held an EGM to dispose of its distribution business and renamed itself as OEL Holdings. The distribution business that it sold made up the bulk of its business – the net asset value of the assets disposed was equal to 92.4 percent of the total net asset value of the group. The base consideration was $70 million.

What did OEL do after the disposal of the bulk of its business? In its 2014 annual report, it said “the Group continued seeking strategic opportunities to inject a new business that could generate and enhance long-term shareholder value.” It attempted to diversify into the oil and gas business. Things went further downhill. The cash balance for the group fell from $24.5 million to $6.2 million between FY2013 and FY2014, then to $1.5 million in FY2015 and down to just $245,000 for FY2016. Between FY2014 and FY2016, the external auditor included an emphasis of matter highlighting material uncertainties that may cast doubt on the company’s and group’s ability to continue as a going concern, although it did not modify its opinion. In other words, rather than enhancing shareholder value, OEL was fighting for survival. On March 23, 2018, OEL announced that the auditor as now included a qualified opinion and a material uncertainty relating to going concern in its report for FY2017.

Therefore, Mr Low was chairman and managing director at OEL as its performance deteriorated markedly. At the same time, he was serving on several other boards as an independent director, most of which have corporate governance or performance issues.

Datapulse shareholders should reflect on the following: Do they have any confidence that Mr Low would be able to lead the Datapulse board in improving its corporate governance and increasing shareholder value, given his track record? The other three directors of Datapulse, including two independent directors, all with no prior experience as listed company directors and no background in the new business that Datapulse is diversifying into, will now be led by him as the company embarks on its diversification into new businesses. I would much rather have a different, more experienced and proven board leading Datapulse in any diversification strategy. The current board has questioned the suitability of some of the proposed directors. It is rather ironic given the experience and track record of the current board, and with a chairman who could not even make the correct disclosures as required by the listing rules. Having said that, I had previously written that few directors would put themselves forward in the situation that Datapulse finds itself in, where requisitioning shareholders are trying to remove the existing directors and appoint new ones. It is too confrontational for most

directors. Therefore, the proposed slate of directors may also not necessarily be what is best for the company going forward. But between the current board and the proposed slate, there is no comparison.

I believe if the requisitioning shareholders are successful in removing the current directors and appointing the proposed directors, the new directors should review the board composition to ensure that they have the best people possible to take the company forward. This may mean some of these newly appointed directors relinquishing their positions rather quickly to make way for a fully functional and effective board. They would then be truly acting in the best interest of the company and all shareholders.

Why the other directors should also be removed

The other two independent directors should also be removed. Ordinarily, I would not object to the appointment of independent directors who have no prior experience as directors of listed companies – which is the case for these two other directors – as long as they are individuals who have integrity and the appropriate skills and experience. Otherwise, we will end up just recycling the same directors across different companies. However, this is not an ordinary situation. These two individuals are not only business associates of the new controlling shareholder, Ng Siew Hong, but they participated inapproving the hasty acquisition of Wayco Manufacturing, which is owned by a close business associate of Ms Ng. The acquisition is in substance an interested person transaction and was done without proper due diligence. I have extensively questioned its commercial merits in my articles.

The fact that the board has used every technicality it could find to delay the EGM requisitioned by shareholders, and that it is now considering holding the EGM only four months later and possibly during the peak AGM season, also suggests a lack of regard for the rights and interests of minority shareholders. Shareholders should not support the appointment or retention of directors who do not treat minority shareholders with respect.

Why the board’s diversification plan should be rejected

The board’s diversification plan should be rejected because it made a poor acquisition and the diversification plan seeks to build on this poor acquisition. Shareholders should not throw good money after bad. If the board has been so hasty in making the Wayco acquisition, how can shareholders be confident that it would not repeat this?Why the resolution by the requisitioning shareholders to stop further diversification for now should be supported

Datapulse now has $90 million-plus in cash. A careful study should be undertaken to determine what is the best use for this cash. No one is arguing that Datapulse should just continue doing what it had been doing all these years as its business has clearly been disrupted. A study could determine the areas that Datapulse could diversify into in order to deliver shareholder value and sustainable performance. However, it is also possible that the best decision for shareholders is to sell the company as a going concern or even go through a voluntary liquidation and distribute the cash back to shareholders. Too often, companies diversify into areas that they have no competitive advantage in or where they do not have the necessary capabilities to succeed, leading to destruction of shareholdervalue – when a better decision would have been to return cash to shareholders.

Why the resolutions to appoint the new directors should be supported

The proposed directors are considered in their action. They are not asking shareholders to approve a hastily-concocted diversification plan of their own, but merely asking shareholders to appoint them so that they can ensure that a thorough study is first undertaken before any diversification plan is put to shareholders for approval.Under the circumstances that the company is in, not many good candidates would want to put themselves forward. This is particularly so because the odds are stacked against them to begin with – given the 29 percent versus 16 percent votes that each side is assured of getting. They know there is a good chance that they will lose if the other minority shareholders do not support them. I am pleased that they have stepped forward. At least, shareholders get to vote on their appointment. The same cannot be said about the current directors.

If they succeed, I would certainly urge them to review the board composition again to ensure that the best directors are appointed to take the company forward.

Biography of Associate Professor Mak Yuen Teen

MAK YUEN TEEN is an associate professor of accounting at the NUS Business School, National University of Singapore, where he teaches corporate governance. He holds first class honours, master and PhD degrees in accounting and finance and is a fellow of CPA Australia. He was the founder and director of the first corporate governance centre in Singapore at the National University of Singapore. Over the past 10 years, Prof Mak has also held positions of Asia-Pacific or Singapore head of research in major consulting firms.Prof Mak has served on key corporate governance committees in Singapore developing and revising codes of corporate governance for listed companies and not-for-profit organisations. He has also been involved in developing several corporate governance ratings and scorecards and has chaired judging panels for corporate governance-related awards in Singapore and the region.

Prof Mak is an active researcher, commentator, speaker and advocate on corporate governance. He has published reports on topics such as corporate governance of banks and insurance companies, board diversity, governance of company groups, annual general meetings, and executive and director remuneration. He is regularly engaged by regulators, companies and other organisations to teach/facilitate workshops for directors, regulators and other industry professionals in Singapore and the region, and has also led governance reviews for listed companies and not-for-profit organisations.

Prof Mak has served on boards of several large not-for-profit organisations in Singapore, including as board chairman, and on audit committees of large not-for-profit organisations in Singapore and in UN funds based in New York. He also served as a member of the Governing Council of the Singapore Institute of Directors from 2000 to 2005. In 2014, he received the Corporate Governance Excellence Award from the Securities Investors Association (Singapore) for his contributions to corporate governance in Singapore, becoming only the second individual to receive this award. In 2015, he received the Excellence in Corporate Governance Award from the Minority Shareholders Watchdog Group in Malaysia for his contributions to corporate governance in the region. That same year, he was recognised by the Singapore Institute of Directors as a Corporate Governance Pioneer in Singapore.

For more information on Prof Mak’s work, visit www.governanceforstakeholders.com.

Comments

Post a Comment